Parameters tab on Life Cycle Cost Dialog

Provides inputs related to the overall life-cycle cost analysis. It establishes many of the assumptions used in computing the present value. It is important that when comparing the results of multiple simulations that the fields in the Parameters objects are the same for all the simulations. To help check this is the case, the first table in the Life-Cycle Cost Report shows the inputs to this object.

An identifying name this LCC analysis.

The field specifies if the discounting of future costs should be computed as occurring at the end, the middle or the beginning of each year. The most common discounting convention uses the end of each year, therefore without a specific reason, the end of year should be used. The year being used starts with the base year and month (see below) and repeats every full year.

All costs assumed to occur during that duration are accumulated and shown as an expense either at the beginning, middle or end of the year. The options are:

Note: Specifically, some military projects may require using the middle of each year.

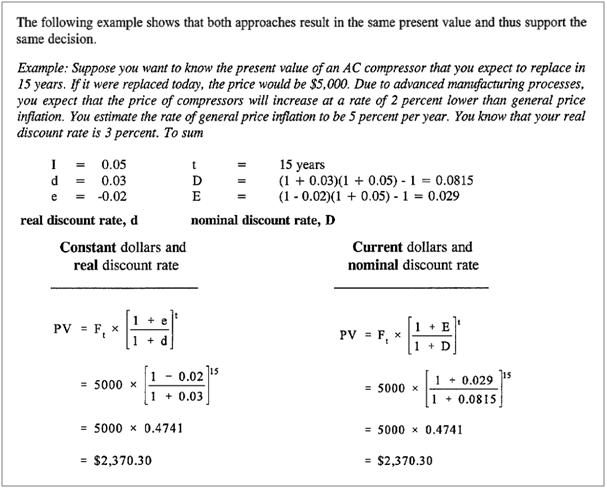

This field is used to determine if the analysis should use constant dollars or current dollars which is related to how inflation is treated. The two options are:

If 1-ConstantDollar is selected, then the Real discount rate input (see below) is used and it excludes the rate of inflation. If 2-CurrentDollar is selected, then the Nominal discount rate (see below) input is used and it includes the rate of inflation. For most analyses, using the 1-ConstantDollar option will be easier since the effect of inflation may be ignored.

Reference: From NIST Handbook 135: “The constant dollar approach has the advantage of avoiding the need to project future rates of inflation or deflation. The price of a good or service stated in constant dollars is not affected by the rate of general inflation. For example, if the price of a piece of equipment is $1,000 today and $1,050 at the end of a year in which prices in general have risen at an annual rate of 5 percent, the price stated in constant dollars is still $1,000; no inflation adjustment is necessary. In contrast, if cash flows are stated in current dollars, future amounts include general inflation, and an adjustment is necessary to convert the current dollar estimate to its constant-dollar equivalent. This adjustment is important because constant- and current-dollar amounts must not be combined in an LCCA.”

Enter the real discount rate as a decimal, e.g. for a 3% rate, enter the value 0.03. This input is used when the Inflation approach is 1-ConstantDollar. The real discount rate reflects the interest rates needed to make current and future expenditures have comparable equivalent values when general inflation is ignored. When the Inflation approach is set to 2-CurrentDollar this input is ignored.

Enter the nominal discount rate as a decimal, e.g. for a 5% rate, enter the value 0.05. This input is used when the Inflation approach is 2-CurrentDollar. The nominal discount rate reflects the interest rates needed to make current and future expenditures have comparable equivalent values when general inflation is included. When Inflation approach is set to 1-ConstantDollar this input is ignored.

Enter the rate of inflation for general goods and services as a decimal, e.g. for a 2% rate, enter the value 0.02. When Inflation approach is set to 1-ConstantDollar this input is ignored.

Example: Below is an example from the NIST Handbook 135 1995 edition.

Enter the month that is the beginning of study period, also known as the beginning of the base period. The options are:

Reference: According to NIST 135 “the base date is the point in time to which all project related costs are discounted in an LCCA [life cycle cost analysis]. The base date is usually the first day of the study period for the project, which in turn is usually the date that the LCCA is performed. In a constant dollar analysis, the base date usually defines the time reference for the constant dollars (e.g. 1995 constant dollars). It is essential that you use the same base date and constant-dollar year for all of the project alternatives to be compared. If you set the base date to the date that the LCCA is performed, then the constant dollar basis for the analysis will be the current date, and you can use actual costs as of that date without adjusting for general inflation.”

Enter the four digit year that is the beginning of study period, such as a year expressed in four digits like “2011”. The study period is also known as the base period. See more details in the previous field.

Enter the month that is the beginning of building occupancy. Energy costs computed by EnergyPlus are assumed to occur during the year following the service date. The service date must not be earlier than the Base date. The options are:

Enter the four digit year that is the beginning of occupancy, such as two years after the previously entered year expressed in four digits so example is like “2013”.

Reference: According to NIST Handbook 135: “The service date is the date on which the project is expected to be implemented; operating and maintenance costs (including energy- and water-related costs) are generally incurred after this date, not before.”

Enter the number of years of the study period. It is the number of years that the study continues based on the start at the base date.

The default value is 25 years, and only integers are allowed that indicate whole years.

Reference: According to NIST Handbook 135, “the study period for an LCCA is the time over which the costs and benefits related to a capital investment decision are of interest to the decision maker. Thus, the study period begins with the base date and includes both the planning/construction period (if any) and the relevant service period for the project. The service period begins with the service date and extends to the end of the study period.”

Enter the overall marginal tax rate for the project costs. This does not include energy or water taxes. The single tax rate entered here is not intended to be a replacement of the complex calculations necessary to compute personal or corporate taxes; instead it is an approximate that may be used for a simple analysis assuming a constant tax rate is applied on all costs. The tax rate entered should be based on the marginal tax rate for the entity and not the average tax rate. Enter the tax rate results in present value calculations after taxes. Most analyses do not factor in the impact of taxes and assume that all options under consideration have roughly the same tax impact. Due to this, many times the tax rate can be left to default to zero and the present value results before taxes are used to make decisions. The value should be entered as a decimal value, e.g. for 15% enter 0.15. For an analysis that does not include tax impacts, enter 0.0. The default is 0.

For an analysis that includes income tax impacts, this entry describes how capital costs are depreciated. Only one depreciation method may be used for an analysis and is applied to all capital expenditures. Only analyses that include tax impacts need to select a depreciation method. The options are:

Depreciation allowances reduce the actual/nominal tax dollars paid by the owner. Thus, analyses using depreciation should be conducted in nominal dollars. For an analysis that does not include tax effects, 11-None should be selected.

Note: For more details about depreciation methods and which one to choose, refer to IRS Publication 946 – How to Depreciate Property. It states that "Depreciation is an annual income tax deduction that allows you to recover the cost or other basis of certain property over the time you use the property. It is an allowance for Fair market value the wear and tear, deterioration, or obsolescence of the Intangible property.” Details on which depreciation method to choose depends on the property being depreciated, IRS Publication 946 and your accountant will be the best sources of information in determining which depreciation method to choose.